Value investing lessons learned and applied from The Intelligent Investor

Benjamin Graham, an economist and investor born in 1894, is widely recognized for the success of one of his disciples – Warren Buffett. However, Graham also contributed some of the best neoclassical investing texts to the financial world. In 1949, he released The Intelligent Investor which later became one of the best-selling value investing books ever.

We touched on The Intelligent Investor in a previous blog post that explored how its principals on value investing applied to penny stock investing. Now we'll explore in more detail the components that Graham and The Bowser Report's founder, R. Max Bowser, preached for successful investing.

This article was adapted from the August 2021 front page article.

Max Bowser and Benjamin Graham

The Intelligent Investor primarily tackles investing principles and psychology. Although the book is 72 years old, Graham’s insight is timeless and many of these principles align with those of Max Bowser, including:

- Focus on the underlying company,

- Utilize of a simple game plan,

- Build wealth (investing is not a get-rich-quick scheme), and

- Lower the frequency of impulse decision-making and emotional mistakes.

Both Bowser and Graham practice the last point by avoiding constantly tracking each stock and watching the markets all hours of the day. Graham mentioned this many times in The Intelligent Investor referring to the stock market as Mr. Market, who is notoriously unpredictable and suspicious. As a result, investors should ignore his sketchy price quotes.

A common example of Mr. Market’s antics is a stock’s quarterly earnings report. Below is a chart showing Apple’s (AAPL) historical earnings statistics:

Out of the 75 earnings events, only 47 of them resulted in share price moving up. Additionally, 31 events resulted in unexpected moves. AAPL is one of the most consistent growth stocks ever and still behaves irrationally during major events. This happens often with Bowser picks due to high expectations for companies with strong fundamentals.

The Formula for Value Investing

There is a reason that The Bowser Report has found success for over 45 years and Graham’s ideologies are timeless – they both adhere to a proven formula. No investment system is complete without a strategy. This applies to a formula for both selecting your investments and executing trades and dollar cost averaging.

One particularly powerful strategy that Graham advocates for is dollar cost averaging, or the practice of spreading out purchases in intervals and equal amounts. This boosts long-term profits and helps to avoid timing the stock market.

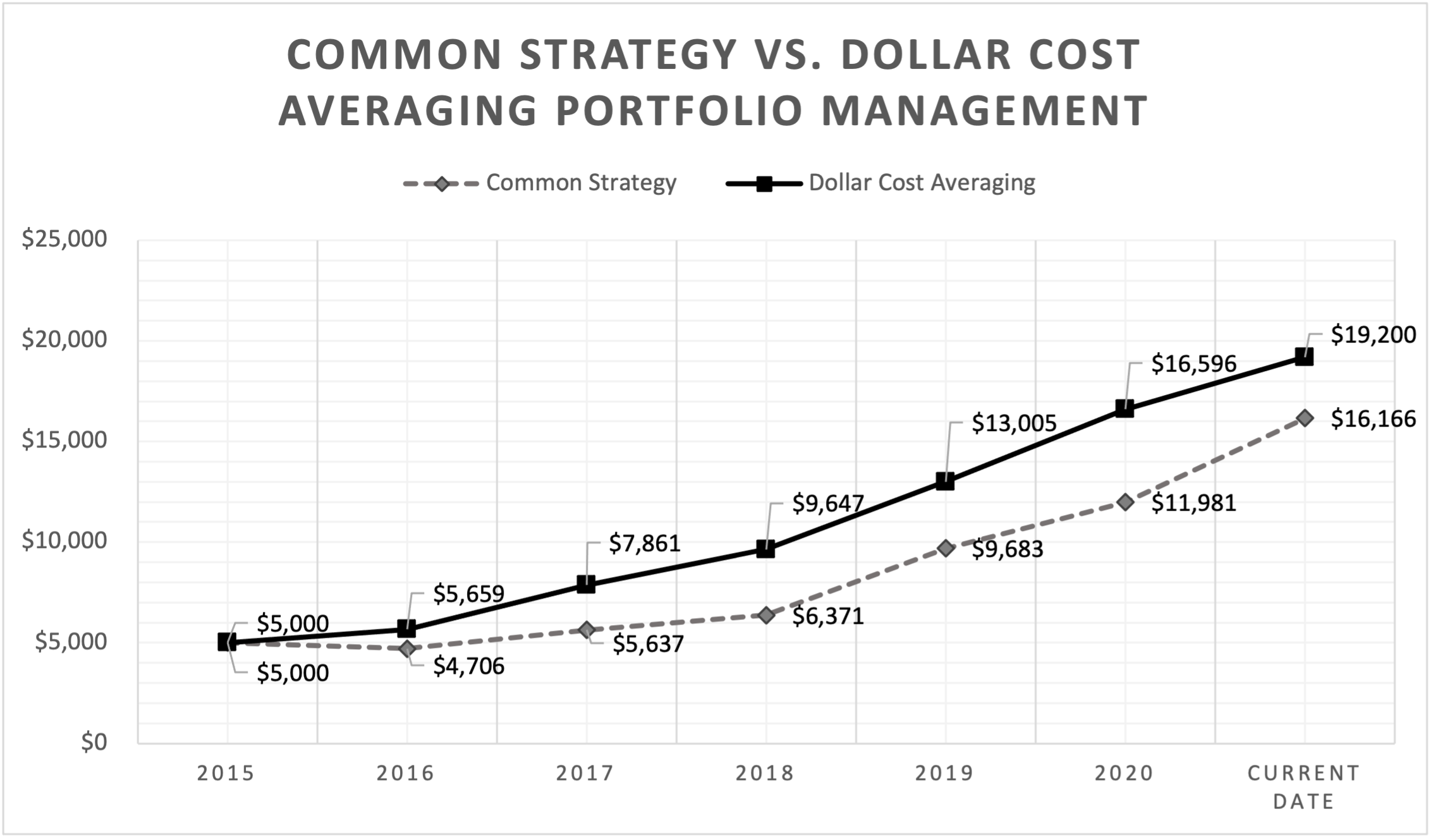

By way of example, consider the Russell 2000 Index ETF (IWM). A common strategy is just two different entry points with the same cost basis of $5,000 ($10,000 total investment). The dollar cost averaging strategy will consist of a $5,000 initial investment and ten purchases of $500 every six months. The chart below shows the portfolio value for both strategies:

The dollar cost averaging strategy performed much better and required much less effort. The one drawback to using this strategy is increased commissions, which has been relatively insignificant since brokerages lowered their rates.

The Bowser Game Plan

Dollar cost averaging is only one aspect of a good formula for portfolio management, and one that is less applicable to Bowser stocks. Trade execution determines profits and losses and can be extremely challenging, which is why we strongly recommend using the Bowser Game Plan, which coincidentally overlaps with many of Graham’s tactics.

The Bowser Game Plan is a great example of a successful formula because of the math behind it. It suggests selling a stock when it doubles, then cutting the remainder loose after a 25% drop from the highest price after doubling. It also suggests selling a stock if it drops 50% before doubling. The simple math that Max Bowser implemented only requires a winning investment less than half of the time, which leads to long-term success. It also encourages cutting losers, letting winners ride and diversification.

Risk Management

Graham highly values a diverse portfolio but warns against too many holdings. He also states that “defensive” investors should maintain a balance of stocks and bonds while “aggressive” investors should focus on equities. The Game Plan suggests maintaining a portfolio of 12-18 holdings. Any number far below or above that range could be detrimental.

Another method Graham uses to limit risk is avoiding hype stocks and IPOs. We wrote about a similar concept in the July 2020 monthly issue, which discussed hype stocks and showed their inability to hold gains.

Similarly, Graham believes the popularity of IPOs makes them more overvalued and hurts the average investor. A big factor in their overvaluation is that the company going public intends to cash out its proceeds from the offering, which can lead to secondary offerings down the road. Below is a chart showing the total proceeds from IPOs over the years:

Management will always prioritize the company over its shareholders as soon as the company goes public. The fact of the matter is that hype will usually cause a temporary overvaluation for a stock or industry.

Picking Value Stocks

Picking a stock relies on finding a valuable company with strong fundamentals and earnings stability. Graham's rationale for investing in companies with healthy financials is based on their earnings track records. Similarly, the Bowser system prioritizes stocks with consistent growth in sales and earnings.

While The Intelligent Investor does not recommend investing in small stocks, it highly recommends companies with a healthy balance sheet. Graham broadly defined a healthy balance sheet as current assets being double that of current liabilities, which is similar to the Bowser Rating's ideal.

Lastly, Graham gravitates to value stocks and companies with a healthy price/earnings (P/E) ratio. A P/E ratio of under 15 is ideal as long as it is accompanied by a reasonable price/book (P/B) ratio. His criteria for this was that if the stocks P/E ratio multiplied by the P/B ratio was less than 22.5, you could buy.

In conclusion, The Intelligent Investor provides readers with helpful value investing methods and a great perspective. Understanding Graham’s approach to both picking stocks and managing a portfolio can assist with investment decisions. If you focus on the underlying company and ignore Mr. Market’s mood swings, your portfolio should thrive.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment